Major averages added over 6% this week despite the fact that there were only a couple of days when stock prices actually rose. Still, that was all markets needed to show yet another big weekly gain as this rally continues to drive stock prices steeply higher.

The biggest catalyst occurred on Monday when the Treasury provided details on the plan to remove toxic assets from bank balance sheets. Investors loved it, stocks rocketed upward and that positive sentiment helped carry stocks most of the week.

In terms of economic reports, investors accepted the 6.3% decline in GDP as better than expected and the usual 650,000 jobless claims as "in line". There was debate over whether housing is improving as seasonal factors and plunging prices are beginning to generate a few purchases here and there. Specifically, existing home sales in February rose 5.1% month-over-month and February new home sales increased 4.7% month-over-month. As many commentators, including Barry Ritholtz, often point out, the month-over-month numbers are seldom instructive; it is the year-over-year numbers that are important because the housing market is susceptible to such deep seasonality. Looked at from the year-over-year point of view housing is still deep in the doldrums with new home sales, for example, still down over 40% from February 2008. Furthermore, there remains more that 12 months of outstanding inventory that will continue to pressure new home sales. By no means are we out of the woods in the housing sector but investors are beginning to think things won't get much worse and indeed may only improve from here.

The Durable Goods report was another example of low expectations being exceeded to the up side. There was a decent new orders number reported and that was the major focus. Shipments and unfilled orders, however, continued to show declines but investors shrugged off those numbers as not sufficently forward-looking. With new orders registering the first improvement in any measure in the Durable Goods report for months, investors were happy to accept it as a sign that things are improving.

And so the rally continued further into short-term over-bought territory. This had the effect of boosting many of the indicators that we track and report as TradeRadar statistics. Let's take a look at this week's results.

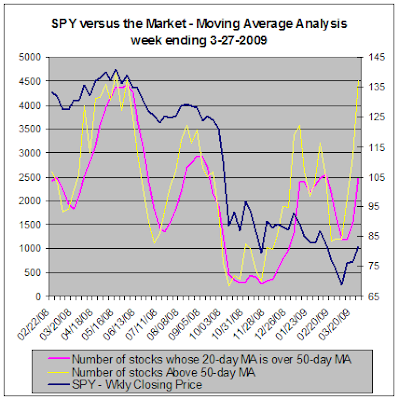

This first chart presents the moving average analysis for the entire market and contrasts it with the performance of the S&P 500 SPDR (SPY). When the number of stocks trading above their 50-day moving average (the yellow line) crosses the line that tracks the number of stocks whose 20-day moving average is above their 50-day moving average (the magenta line) there is an expectation that you will get a change in the trend of the S&P 500.

OK, I would like to interpret this chart as unabashedly bullish but I'm afraid that there are extremes being reached that suggest a pullback is close. With more than 60% of all the stocks we evaluated above their 20-day moving averages we are now at the highest level since summer of 2008. The number of stocks above their 50-day MA is also rapidly increasing though it hasn't hit an extreme level yet; nevertheless, it would appear that prudence and caution are the appropriate watch words after such a quick run-up.

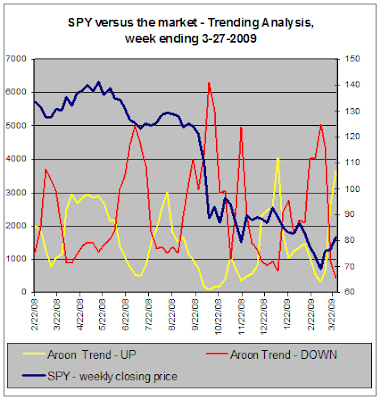

This next chart is based on Aroon Analysis and compares our trending statistics to the performance of SPY. We use Aroon to measure whether stocks are in strong up-trends or down-trends. The number of stocks in down-trends is indicated by the red line and the number of stocks in up-trends is indicated by the yellow line.

Here again the readings are elevated. Though the number of stocks in up-trends hasn't quite exceeded the previous highest level, the number of stocks in down-trends has fallen to the lowest level we have seen since we began tracking these statistics over year ago. Once more, the interpretation is that a pullback is becoming more likely.

This coming week, we'll have a good number of new economic reports which might help confirm whether a bottom is being formed. We start off with Consumer Confidence, then the Case-Shiller Home Price Index, Chicago PMI, the ADP employment report, ISM Index, pending home sales, auto and truck sales, the weekly initial jobless claims number, factory orders, hourly earnings, the Nonfarm Payrolls and Unemployment reports and finally ISM Services.

In other words, we'll get the latest readings on housing, manufacturing, services and employment - pretty much everything that is economically important. If the majority of these reports come in better than expected we could see caution thrown to the wind and further stock price gains.

And don't forget, the G-20 are meeting this week. Discord and disagreement could be unsettling to the markets. On the other hand, it could all be dismissed as political posturing. Given how much the actions of Washington have impacted stock prices lately, though, this meeting could have greater influence than usual.

In the meantime, be careful about rallies inspired by end of month window dressing. There will be better buying opportunities soon enough.

The biggest catalyst occurred on Monday when the Treasury provided details on the plan to remove toxic assets from bank balance sheets. Investors loved it, stocks rocketed upward and that positive sentiment helped carry stocks most of the week.

In terms of economic reports, investors accepted the 6.3% decline in GDP as better than expected and the usual 650,000 jobless claims as "in line". There was debate over whether housing is improving as seasonal factors and plunging prices are beginning to generate a few purchases here and there. Specifically, existing home sales in February rose 5.1% month-over-month and February new home sales increased 4.7% month-over-month. As many commentators, including Barry Ritholtz, often point out, the month-over-month numbers are seldom instructive; it is the year-over-year numbers that are important because the housing market is susceptible to such deep seasonality. Looked at from the year-over-year point of view housing is still deep in the doldrums with new home sales, for example, still down over 40% from February 2008. Furthermore, there remains more that 12 months of outstanding inventory that will continue to pressure new home sales. By no means are we out of the woods in the housing sector but investors are beginning to think things won't get much worse and indeed may only improve from here.

The Durable Goods report was another example of low expectations being exceeded to the up side. There was a decent new orders number reported and that was the major focus. Shipments and unfilled orders, however, continued to show declines but investors shrugged off those numbers as not sufficently forward-looking. With new orders registering the first improvement in any measure in the Durable Goods report for months, investors were happy to accept it as a sign that things are improving.

And so the rally continued further into short-term over-bought territory. This had the effect of boosting many of the indicators that we track and report as TradeRadar statistics. Let's take a look at this week's results.

TradeRadar Alert HQ Stock Market Statistics --

Each week our Alert HQ process scans over 7400 stocks and ETFs and records their technical characteristics. Primarily we look for BUY and SELL signals for our free stock alerts; however, we also summarize the data in order to gain insights in the week's market action. The following charts are based on daily data and present the state of some of our technical indicators.This first chart presents the moving average analysis for the entire market and contrasts it with the performance of the S&P 500 SPDR (SPY). When the number of stocks trading above their 50-day moving average (the yellow line) crosses the line that tracks the number of stocks whose 20-day moving average is above their 50-day moving average (the magenta line) there is an expectation that you will get a change in the trend of the S&P 500.

OK, I would like to interpret this chart as unabashedly bullish but I'm afraid that there are extremes being reached that suggest a pullback is close. With more than 60% of all the stocks we evaluated above their 20-day moving averages we are now at the highest level since summer of 2008. The number of stocks above their 50-day MA is also rapidly increasing though it hasn't hit an extreme level yet; nevertheless, it would appear that prudence and caution are the appropriate watch words after such a quick run-up.

This next chart is based on Aroon Analysis and compares our trending statistics to the performance of SPY. We use Aroon to measure whether stocks are in strong up-trends or down-trends. The number of stocks in down-trends is indicated by the red line and the number of stocks in up-trends is indicated by the yellow line.

Here again the readings are elevated. Though the number of stocks in up-trends hasn't quite exceeded the previous highest level, the number of stocks in down-trends has fallen to the lowest level we have seen since we began tracking these statistics over year ago. Once more, the interpretation is that a pullback is becoming more likely.

Conclusion --

Though the economy is still in recession, the feeling among investors for the last few weeks has been that we have reached a trough. I hope that's true but so far, most economic reports have only confirmed that the decline in indicators of economic health is slowing, not bottoming or improving. It may be easier to catch the falling knife now but for most longer-term investors, there is no good reason the chase this rally.This coming week, we'll have a good number of new economic reports which might help confirm whether a bottom is being formed. We start off with Consumer Confidence, then the Case-Shiller Home Price Index, Chicago PMI, the ADP employment report, ISM Index, pending home sales, auto and truck sales, the weekly initial jobless claims number, factory orders, hourly earnings, the Nonfarm Payrolls and Unemployment reports and finally ISM Services.

In other words, we'll get the latest readings on housing, manufacturing, services and employment - pretty much everything that is economically important. If the majority of these reports come in better than expected we could see caution thrown to the wind and further stock price gains.

And don't forget, the G-20 are meeting this week. Discord and disagreement could be unsettling to the markets. On the other hand, it could all be dismissed as political posturing. Given how much the actions of Washington have impacted stock prices lately, though, this meeting could have greater influence than usual.

In the meantime, be careful about rallies inspired by end of month window dressing. There will be better buying opportunities soon enough.

Comments

Post a Comment